Common Reporting Standard (CRS) Frequently Asked Questions (FAQ’s)

OECD CRS-related Frequently Asked Questions

OECD CRS-related Frequently Asked Questions

IRD CRS-related FREQUENTLY ASKED QUESTIONS

-

- Q: What is the Common Reporting Standard (CRS)?

-

A: The Common Reporting Standard (CRS) is the standard for automatic exchange of financial account information in tax matters, including commentaries thereon approved on 15th July 2014 by the Organization of Economic Co-operation and Development (OECD).

The Common Reporting Standard (CRS) has been implemented into the legislation of Trinidad and Tobago by the enactment of Act 7 of 2020 – Mutual Administrative Assistance in Tax Matters. This Act establishes due diligence and reporting obligations for Reporting Financial Institutions in accordance with the CRS and provides for the exchange of this information with Member States, for the purposes of taxation and matters incidental thereto.

A: ccording to the provisions of this Act, Reporting Financial Institutions are required to identify and report on accounts held by reportable persons.

-

- Q: What is a Financial Institution?

-

A: Financial Institution means a custodial institution, a depository institution, an investment entity, or a specified insurance company.

-

- Q: Are Credit Unions Financial Institutions?

-

A: Yes. A credit union is a Non-Profit Financial Institution controlled by its members.

-

- Q: What institution is classified as a Reporting Financial Institution?

-

A: A Reporting Financial Institution means any Trinidad and Tobago Financial Institution that is not a Non-Reporting Financial Institution. A Reporting Financial Institution includes:

- A Custodial institution- any entity that holds, as a substantial portion of its business, financial assets for the account of others;

- A Depository institution - any entity that accepts depositsin the ordinary course of a banking or similar business;

- An investment entity. An entity —

- that primarily conducts as a business one or more of the following activities or operations for, or on behalf of a customer:

- trading in foreign exchange, interest rate and index instruments, transferable securities or commodities futures trading or money market instruments, such as cheques, bills, certificates of deposits, derivatives;

- individual and collective portfolio management; or

- otherwise investing, administering or managing financial assets or money on behalf of other persons; or

- the gross income of which is primarily attributable to investing, reinvesting, or trading in financial assets, if the entity is managed by another entity that is a depository institution, a custodial institution, a specified insurance company, or an investment entity under paragraph (a), but does not include an entity that is an active Non-Financial Entity (NFE).

- that primarily conducts as a business one or more of the following activities or operations for, or on behalf of a customer:

- A specified insurance company – which means an entity that is an insurance company, or the holding company of an insurance company, that issues or is obligated to make payments with respect to a cash value insurance contract or an annuity contract.

-

- Q: What is a Trinidad and Tobago Financial Institution?

-

A:

- A Financial Institution that is resident in Trinidad and Tobago but excludes any branch of that Financial Institution that islocated outside of Trinidad and Tobago; and

- any branch of a Financial Institution, if that is not a resident in Trinidad and Tobago.

-

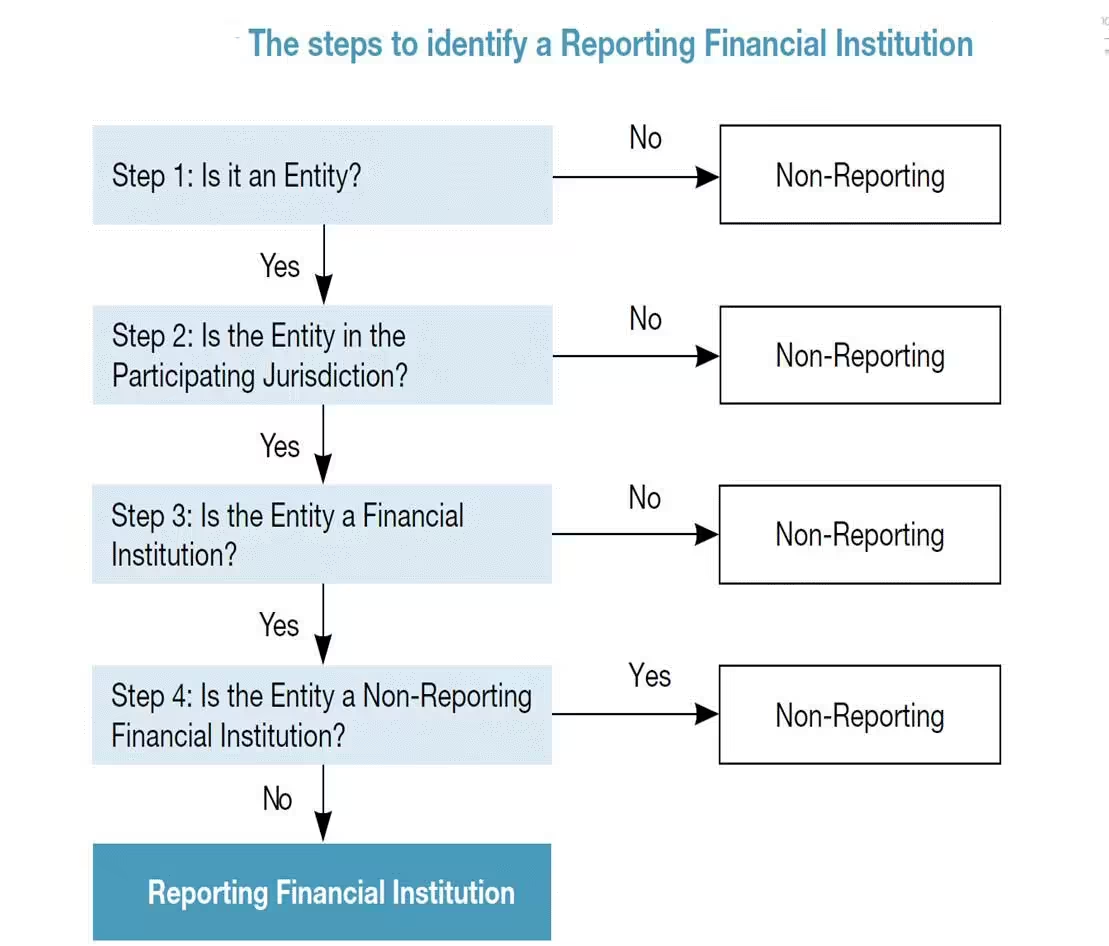

- Q: What are the steps to identify a Reporting Financial Institution?

-

A:

-

- Q: What is an entity?

-

A: An entity means a legal person or legal arrangements such as a corporation, partnership, trust, or foundation.

-

- Q: What is a Reportable Jurisdiction Financial Institution?

-

A: A Reportable Jurisdiction Financial Institution is –

- any Financial Institution that is resident in a jurisdiction but excludes any branch of that Financial Institution that is located outside such jurisdiction; and

- any branch of a Financial Institution that is not resident in a jurisdiction, if that branch is located in such jurisdiction.

-

- Q: What is a Non-Reporting Financial Institution?

-

A: A Non-Reporting Financial Institution means any Financial Institution that is –

- a Governmental Entity, International Organisation or Central Bank, other than with respect to a payment that is derived from an obligation held in connection with a commercial, financial activity of a type engaged in by a specified insurance company, custodial institution, or depository institution;

- a broad participation retirement fund; a narrow participation retirement fund; a pension fund of a Governmental Entity, International Organisation or Central Bank; or a qualified credit card issuer;

- any other entity that presents a low risk of being used to evade tax has substantially similar characteristics to any of the entities described in paragraphs (a) and (b), and is defined in domestic law as a non-reporting Financial Institution, provided that the status of such entity as a non-reporting Financial Institution does not frustrate the purposes of the Common Reporting Standard;

- an exempt collective investment vehicle; or

- a trust to the extent that the trustee of the trust is a Reporting Financial Institution and reports all information required to be reported under this act with respect to all Reportable Accounts of the trust;

-

- Q: What is a Non-Financial Entity (NFE)?

-

A: An NFE means an entity that is not a Financial Institution.

-

- Q: What is a Reportable Account?

-

A: A Reportable Account means an account held by one or more Reportable Persons or by a Passive NFE with one or more controlling persons that is a Reportable Person, provided it has been identified as such pursuant to the Common Reporting Standard Due Diligence Requirements described in Schedule 1. Reportable Accounts are Financial Accounts maintained by a Reporting Financial Institution that is not an Excluded Account. Reportable Account includes:

- a Depository Account

- a Custodial Account

- in the case of an Investment Entity, any equity or debt interest in the Financial Institution but does not include any Equity or Debt Interest in an entity that is an investment entity solely because it—

- renders investment advice to, and acts on behalf of; or

- manages portfolios for and acts on behalf of a customer for the purpose of investing, managing, or administering Financial Assets deposited in the name of the customer with a Financial Institution other than such entity;

- in the case of Financial Institutions not described in paragraph (a), any Equity or Debt Interest in the Financial Institution, if the class of interests was established with a purpose of avoiding reporting in accordance with Section 12(3); and

- Any Cash Value Insurance Contract And Any Annuity Contract Issued Or Maintained By A Financial Institution, Other Than A Non-Investment Linked, Non-Transferable Immediate Life Annuity That Is Issued To An Individual And Monetises A Pension Or Disability Benefits Provided Under An Account That Is An Excluded Account;

- Q: What is an Excluded Account?

-

A: Refer to Section 4(1) of Act 7 of 2020 – Mutual Administrative Assistance in Tax Matters, for the definition of Excluded Account.

-

- Q: What is a Pre-existing Account?

-

A: A Pre-existing Account means a financial account maintained by a Reporting Financial Institution as of 31 December 2024.

-

- Q: What is a New Account?

-

A: A New Account means a Financial Account maintained by a Reporting Financial Institution opened on or after 1 January 2025.

-

- Q: What is a Pre-existing Individual Account?

-

A: A Pre-existing Individual Account means a Pre-Existing Account held by one or more individuals.

-

- Q: What is a New Individual Account?

-

: A New Individual Account means a new account held by one or more individuals.

-

- Q: What is a New Entity Account?

-

A: A New Entity Account means a new account held by one or more Entities.

-

- Q: What is a Pre-existing Entity Account?

-

A: A Pre-Existing Entity Account means a Pre-existing account held by one or more Entities.

-

- Q: What is a Lower Value Account?

-

A: A Lower Value Account means a Pre-existing Individual Account with a balance or value as of the date to be prescribed that does not exceed one million United States dollars.

-

- Q: What is a High-Value Account?

-

A: A High-Value Account means a Pre-existing Individual Account with a balance or value that exceeds one million dollars as of the date to be prescribed or the prescribed date of any subsequent year.

-

- Q: Who is a Reportable Person?

-

A: A Reportable Person means a Reportable Jurisdiction Person who is not—

- a corporation, the stock of which is regularly traded on one or more established securities market;

- any corporation that is a related entity of a corporation described in paragraph (a);

- a Government Entity;

- an International Organisation;

- a Central Bank; or

- a Financial Institution

-

- Q: Who is a Reportable Jurisdiction Person?

-

A: A Reportable Jurisdiction Person means an individual or entity that is Resident in a Reportable Jurisdiction under the tax laws of such jurisdiction or an estate of a decedent that was resident of a reportable jurisdiction and where an entity such as a Partnership, Limited Liability Partnership or similar legal arrangement has no residence for tax purposes it shall be treated as Resident in the jurisdiction in which its place of effective management is situated

-

- Q: What information is required to be reported under the CRS?

-

A: Reporting Financial Institutions are required to report the following information with respect to each Reportable Account.

- The name, address, jurisdiction(s) of residence, TIN(s) and date and place of birth (in the case of an individual) of each Reportable Person that is an account holder of the account and, in the case of any Entity that is an account holder and that, after application of the due diligence procedures consistent with Sections V, VI and VII, is identified as having one or more controlling Persons that is a Reportable Person, the name, address, jurisdiction(s) of residence and TIN(s) of the entity and the name, address, jurisdiction(s) of residence, TIN (s) and date and place of birth of each Reportable Person.

- The account number (or the functional equivalent in the absence of an account number).

- The name and identifying number (if any) of the Reporting Financial Institution.

- The account balance or value (including, in the case of a Cash Value Insurance Contract or Annuity Contract, the Cash Value or surrender value) as of the end of the relevant calendar year or other appropriate reporting period or, if the account was closed during such year or period, the closure of the account.

- In the case of any Custodial Account:

- the total gross amount of interest, the total gross amount of dividends, and the total gross amount of other income generated with respect to the assets held in the account, in each case paid or credited to the account (or with respect to the account) during the calendar year or other appropriate reporting period; and

- the total gross proceedsfrom the sale or redemption of financial assets paid or credited to the account during the calendar year or other appropriate reporting period with respect to which the Reporting Financial Institution acted as a custodian, broker, nominee, or otherwise as an agent for the Account Holder.

- In the case of any Depository Account, the total gross amount of interest paid or credited to the account during the calendar year or other appropriate reporting period.

- In the case of any account not described in subparagraph A (5) or (6), the total gross amount paid or credited to the Account Holder with respect to the account during the calendar year or other appropriate reporting period with respect to which the Reporting Financial Institution is the obligor or debtor, including the aggregate amount of any redemption payments made to the Account Holder during the calendar year or other appropriate reporting period.

-

- From what year(s) is CRS reporting required?

-

A: CRS Information isrequired to be reported/exchanged with respect to the calendar year 2025 and all subsequent years.

-

- Q: When is the due date for Reporting Financial Institutions to submit CRS Reports to the BIR?

-

A: CRS Reports are to be submitted to the BIR on or before 31 May of the year following the calendar year to which the information relates in respect of every Reportable Account maintained by the institution.

Note: Financial Institutions are encouraged to submit their reports as early as possible.

-

- Q: Who can submit CRS Reports for a Reportable Financial Institution?

-

A: An Administrator or authorized Point of Contact (PoC) for the FI can submit CRS Reports. An Administrator is an employee of a Financial Institution who is authorized to manage the company’s tax profile Inland Revenue Division CRS system. The Administrator can give/revoke access to the PoCs in respect of the company’s tax accounts on Inland Revenue Division CRS System.

The Administrator and PoCs will need to have BIR numbers.

-

- Q: Does the CRS Administrator need to be registered with the Board of Inland Revenue (BIR)?

-

A: Yes. An Administrator authorized by a Financial Institution will need to register with the Board of Inland Revenue. BIR numbers are required to authenticate users accessing Inland Revenue Division CRS system.

-

- Q: How does the Administrator register with the Board of Inland Revenue to upload CRS Reports on the Inland Revenue Division CRS system?

-

A: See the registration guide in relation to information on registering an Administrator with the Board of Inland Revenue located at http://www.ird.gov.tt/international-tax

-

- Q: Who notifies the Account Holder that information relating to that person was sent to the Board and will be exchanged with the competent authority of an applicant State in accordance with the Mutual Administrative Assistance in Tax Matters Act 7 of 2020?

-

A: Reporting Financial Institutions must notify the account holder by 31st January in the calendar year following the first year in which the account held by the person became reportable.

-

- Q: Is an offence committed if the requirements and regulations of Act 7 of 2020 - (Mutual Administrative Assistance in Tax Matters) is not adhered to?

-

A: Yes, an offence is committed as follows -:

Where persons enter into arrangements where the main purpose is considered to be an avoidance of the requirements and regulations of this Act, commits an offence and is liable -:

- on summary conviction to a fine of three hundred thousand dollars ($300,000.00) and imprisonment for one year (1yr); and

- on conviction on indictment to a fine of six hundred thousand dollars ($600,000.00) and imprisonment for two years(2yrs)

- Non-Compliance by Reporting Financial Institutions A Reporting Financial Institution (RFI) commits an offense if it fails to meet its operational obligations. This includes:

- Failure to Keep Records: Not maintaining records for at least five years as required under Section 17.

- Reporting Failures: Failing to file required information or failing to file it on time.

- Due Diligence Failures: Failing to carry out mandated due diligence, including the failure to obtain self-certifications.

- False Reporting: Providing a false statement or report to the Board.

- Penalty: RFIs are liable to a penalty of $100,000 for these offenses.

- If the RFI is a legal arrangement (like a trust) or a branch, the persons responsible for managing its affairs (directors, trustees, etc.) are liable for the penalty.

-

- Q: How long does the Reporting Financial Institution need to keep records?

-

A: A Reporting Financial Institution is required to keep records for a period not less than five (5yrs) after the end of the period in which the information is required to be reported under Schedule 1.

-

- Q: What are the Due Diligence Requirements?

-

A: Refer to Schedule 1 of Act 7 of 2020 (Mutual Administrative Assistance in Tax Matters) for the Common Reporting Standards and Due Diligence requirements.

-

- Q: Can Reporting Financial Institutions employ the use of service providers in order to fulfil their reporting and due diligence obligations under this Act?

-

A: Yes, Reporting Financial Institutions are allowed to employ service providers in order to fulfill their reporting and due diligence requirements as detailed in Schedule I of the Act. The Reporting Financial Institution shall be ultimately responsible for the reporting and due diligence requirements under the Act.

-

- Q. Where can I access more details on aforementioned FAQ’s?

-

A: Refer undermentioned legislation link for Act 7 of 2020 – Mutual Administrative Assistance in Tax Matters under header of Common Reporting Standard (CRS)

-

- Q: Where can I find more information on the Common Reporting Standard (CRS)?

-

A: Refer to the following link:

https://www.oecd.org/n/networks/global-forum-tax-transparency/resources/aeoi-implementation-portal.